COVID-19 has hit UK businesses across all sectors, and the outbreak of the pandemic has even overshadowed Brexit. Findings from GlobalData’s 2020 UK SME Insurance Survey indicate that SMEs are far more concerned about loss of business due to coronavirus than the risks associated with Brexit. More than ever, insurers will need to adapt their products and cover to support and protect SMEs in line with the changing risks that they face after the pandemic.

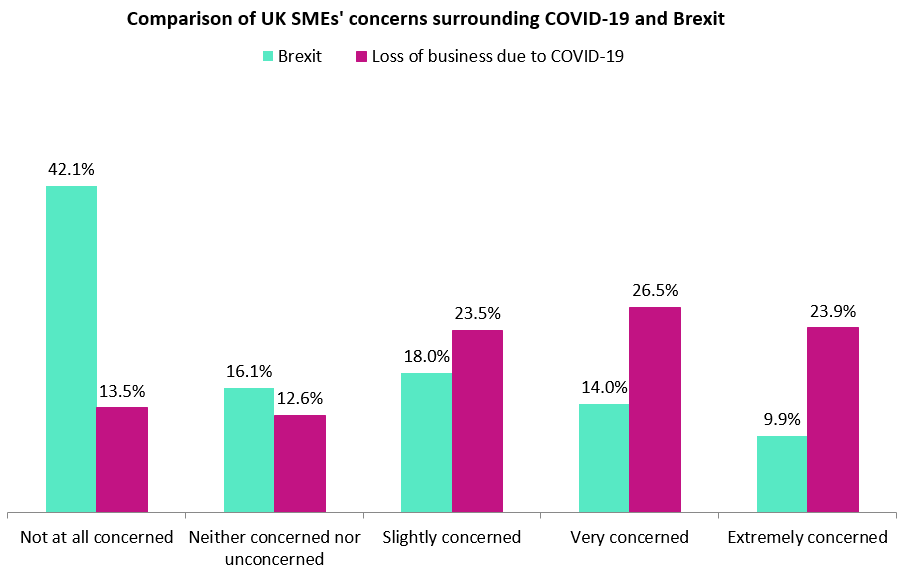

The majority of UK SMEs (73.9%) are concerned to some extent by the prospects of loss of business due to the pandemic, as per GlobalData’s 2020 UK SME Insurance Survey. Moreover, half of all SMEs are either very concerned or extremely concerned by this. Meanwhile, 41.9% of SMEs cited to be concerned about Brexit. Many SMEs have already incurred financial losses as a result of the unexpected COVID-19 outbreak, while the potential impact of Brexit has loomed ever since the 2016 referendum, leaving businesses with more time to make adjustments and prepare.

Go deeper with GlobalData

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

The lockdown measures enforced by the government at the onset of the pandemic have significantly affected the operations of many SMEs, which now face the prospect of a second national lockdown or at least enhanced social distancing measures.

Non-essential businesses have had to close temporarily or continue operating remotely. As such, many employees have continued to work from home, forcing businesses to rely more heavily on technology yet also leaving them more exposed to cyber risks.

Traditionally, the uptake of cyber insurance has been greater among larger corporations, but the pandemic opens a window of opportunity to insurers as the need for this kind of protection mounts among SMEs. In contrast, as employees work from home more often, some businesses may end up reducing the footprint of their physical offices. In turn, this is bound to reduce the coverage limits required by businesses, thus lowering premiums and reducing the size of the commercial insurance market.

Business interruption policies that provide cover for notifiable diseases have attracted a lot of interest since the COVID-19 outbreak, but offering such coverage can be risky for insurers. Some of them have avoided liability, indicating that these policies were never intended to provide cover for lost income due to pandemics. It therefore leaves scope for clearer policy wordings and better designed policies to be more prepared in the advent of future catastrophic events, if not future waves of COVID-19.

For instance, partnerships with governments or the formation of a scheme similar to Pool Re could allow insurers to share their risk and create products that offer better protection to SMEs.