The growing effects of climate change are impacting all parts of the world in a multitude of ways. The increase in natural hazards – from floods to wildfires – are causing concern for insurers across many countries, including the US. Wildfires and hurricanes have become more prominent in recent years and insurers are having to mitigate these threats by increasing premiums on the whole.

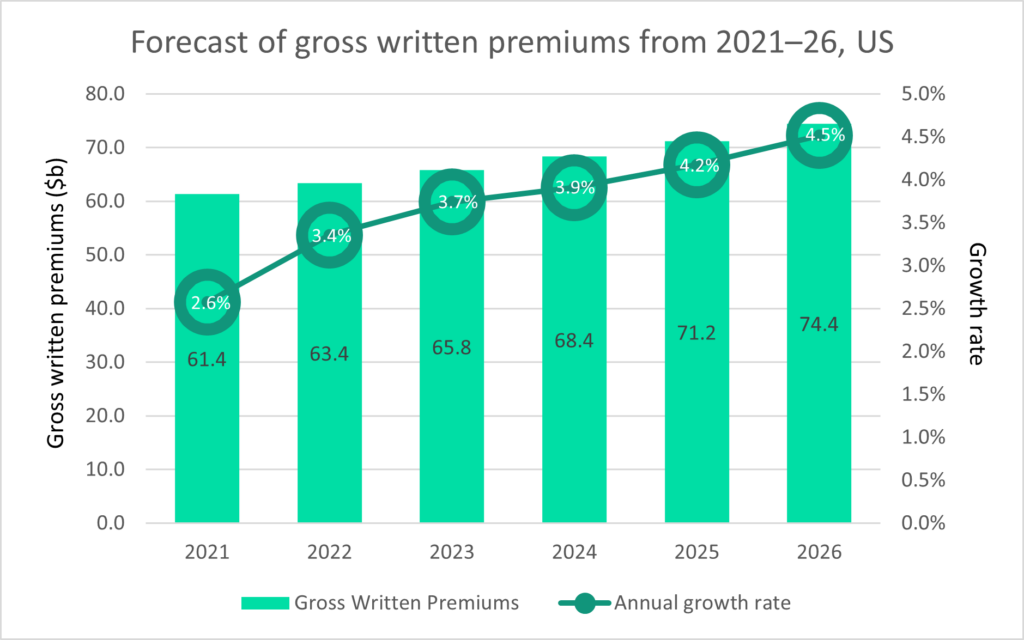

The increased likelihood of natural disasters, paired with the increasing cost of reinsurance, means insurers are having to charge more on premiums. This can be seen in GlobalData’s forecast for gross written premiums (GWP) in the US relating to fire and natural hazards. GWP is set to record a compound annual growth rate of 3.9% from 2021 to 2026. GWP is expected to grow from $61.4bn in 2021 to $74.4bn in 2026 – an increase of 21.3%. This can be attributed to the adverse effects of climate change causing an increase in claims relating to fire and natural hazards.

Go deeper with GlobalData

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

In response, insurers are inflating premiums to cover the cost. In 2021, the insurance industry covered 41.1% ($111m) of global economic losses caused by natural disasters. Losses in 2021 increased by 22.9% compared to 2020, and certain categories (such as storms and wildfires) showed major cost increases.

Over the next century, the Intergovernmental Panel on Climate Change predicts a global temperature rise of 2.5–10°F. According to the report, the net costs of climate change are anticipated to be large and will rise over time. The implications for insurance are significant. Rising sea levels cause floods all across the world, leading to an increase in commercial and personal property claims. Indeed, severe weather events have been one of insurers’ top concerns, with an increase in the frequency of wildfires, typhoons, hurricanes, and storms around the world — resulting in larger claims payouts.

Every year, the beginning of June marks the start of hurricane season across the Americas. While forecasters may try to estimate how many named storms will hit Florida and how strong each one will be, nothing is ever definite. However, the National Oceanic and Atmospheric Administration and a team from Colorado State University anticipate that activity in 2022 will be “far above average” with 20 named storms, 10 of which will become hurricanes and five major hurricanes. According to Munich Re, overall losses from the 2021 hurricane season in the US amounted to $65bn (including damage from flooding), of which $36bn was insured.

Homeowners across Florida are faced with lots of unpredictability as premiums and deductibles are fluctuating. Premiums are increasing in Florida due to a roofing scam, doubling the cost of claims for insurers. In addition, storm hardening initiatives may result in an increase in monthly utility charges, which tied into the rapid inflation being experienced in the US will have an effect on homeowners’ financial wellbeing. As a result, some insurers are losing clients. The predictions ahead, as well as previous records of the economic losses caused by hurricanes, highlight the importance of homeowners conducting an insurance “check-up” with their agent. Doing so will allow them to take stock of their coverage to ensure they are adequately protected against damages caused by natural disasters.