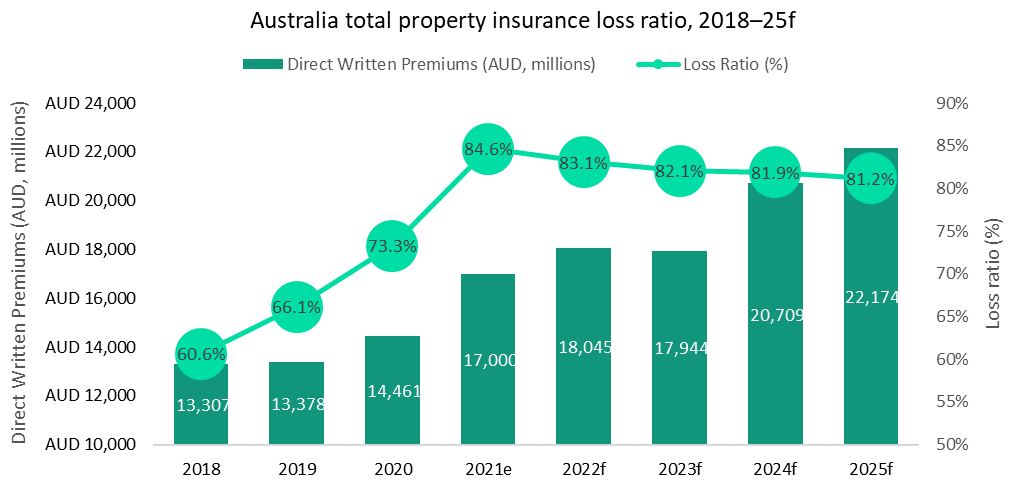

The announcement of a government-backed cyclone reinsurance scheme in Australia will help insurers to keep on top of a growing loss ratio in the total (commercial and residential) property insurance market. The loss ratio in the market has been growing since 2018 and is expected to reach 84.6% in 2021 from 60.6% in 2018.

According to GlobalData’s Global Insurance Database, the loss ratio in the total property insurance market in Australia is expected to reach 84.6% in 2021, up 11.3 percentage points from 2020. A growing loss ratio will squeeze profitability as a greater proportion of premium income is spent on claims. This loss ratio increase comes despite a 17.6% growth in direct written premiums in 2021, totaling AUD17,000 million ($12,143 million). Given that GlobalData forecasts the total property insurance market to grow to AUD22,174 million ($15,838 million) by 2025, and that the loss ratio is forecast to remain over 80%, it is clear that severe claims will continue to burden insurers in the line, with much of this accounted by adverse weather-related claims.

Go deeper with GlobalData

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

The Insurance Council of Australia has welcomed the release of draft legislation to set up a government-backed cyclone reinsurance scheme as it will help to create a long-term and sustainable market. The AUD10bn ($7.1bn) reinsurance pool will allow insurers to continue offering adequate cover and affordable premium prices for consumers in cyclone-threatened areas, particularly in the more cyclone-prone areas of Northern Australia where the risk is generally larger. The increasing damage and threat caused by climate change-induced weather patterns across the world will reinforce the need for such schemes elsewhere. The success of the government-backed Flood Re in the UK will give confidence to other governments of the viability of such arrangements.

The weather in Australia in 2021 has been littered with significant events. A series of adverse weather events across the year have led to a huge number of claims. In March, large parts of New South Wales were hit by ‘one-in-50-years’ flooding, with 18,000 people evacuated from their homes. In April, a category-three cyclone (Seroja) hit Western Australia, with some 70% of structures damaged in one town, home to 1,500 people. In October, tornadoes damaged property in Queensland and New South Wales, with the former seeing record-sized hailstones (16cm in diameter) as well. A La Niña summer has been declared, meaning the coming summer is set to be cooler, wetter, and stormier than average. Indeed, leaked cabinet documents reveal there is an increased chance of widespread flooding, coastal flooding and erosion, and tropical cyclones in certain areas, particularly the East and South-East of the country.

On top of the risk of cyclones, insurers can help their customers in dealing with the threat of flooding and climate change by promoting flood defence in newly built properties. Properties in high-risk areas should be equipped with flood resistance equipment, such as removable barriers, in expectation of future events driven by climate change. This will serve to limit the damage that adverse weather (especially flooding) can cause to properties, reducing claims and easing the burden on insurers.