GlobalData surveying indicates that many consumers looking to switch insurance providers are actually struggling to find better deals despite rampant premium hikes in many personal lines. The news that MoneySuperMarket announced record annual revenue from its insurance division in 2023, up 28% in 2022, shows the challenge insurers face in competing on price in such a value-driven market. With premiums at record levels and such a significant proportion of consumers looking to switch (even if many cannot), the aggregator has seen such impressive results through higher commissions and improved conversion rates.

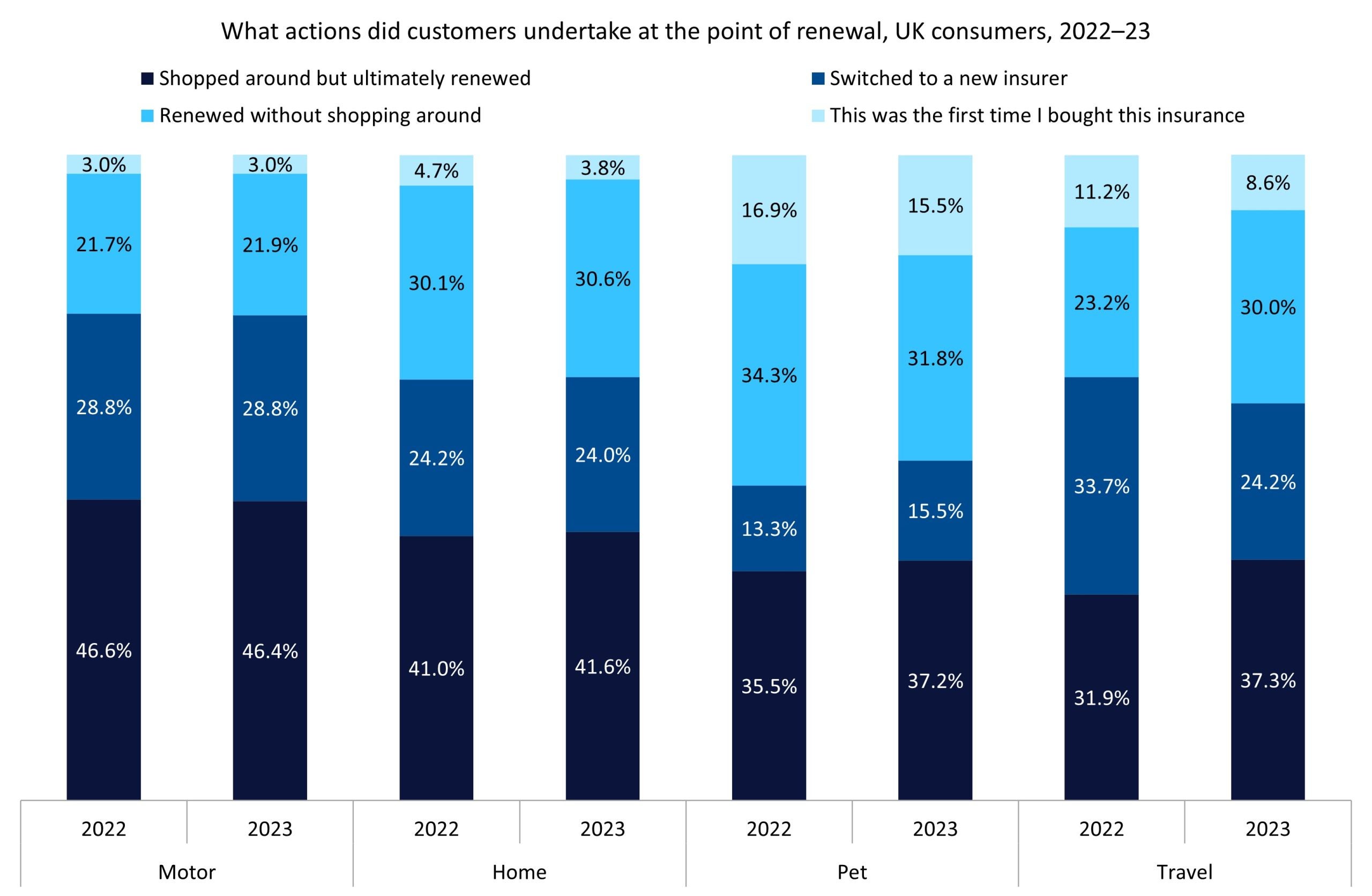

Price comparison websites (PCWs) are uniquely positioned to take advantage of spiralling insurance premiums in the post-pandemic world. According to GlobalData’s 2023 UK Insurance Consumer Survey, more than 50% of UK insurance customers shopped around before either switching or renewing with their insurer. Premiums in the motor and home lines have risen significantly in the past two years. Data from the Association of British Insurers (ABI) indicates the average premium increased by 33.5% between Q4 2022 and Q4 2023. For combined, buildings-only, and contents-only policies, these increases were 19.1%, 21.9%, and 12%, respectively.

Go deeper with GlobalData

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

Given these hefty price rises (in conjunction with the myriad of other extra costs passed on to consumers in the past few years), it is no surprise that so many individuals are seeking better deals on their insurance. In the motor line, 75.2% of customers shopped around before renewing or switching their policy. Just over one-third of this group found a cheaper provider and switched. These figures are largely similar to 2022, suggesting a stable and competitive market as many consumers were unable to find better deals even when actively searching. Similar findings were seen in the home line, with 65.6% of consumers shopping around in 2023; again, just over one-third of this cohort were able to find an alternative and switch.

Strong competition across personal lines, accompanied by spiralling costs (in both claims and operating expenses), has put huge pressure on insurers. RSA’s exit from UK personal lines shows that even the largest players are struggling to keep up with these costs. In 2022, RSA was the second-largest home insurance provider, with an 11.3% market share as per GlobalData’s UK Top 25 General Insurance Competitor Analytics. Insurance has always been a value-driven market—more than 60% of all switchers did so due to a lower premium from their new insurer—and the cost-of-living crisis has pushed even more consumers to squeeze the utmost value from their products. The trend of financially constrained consumers seeking better deals on their insurance (or cancelling altogether) will surely continue in 2024. Insurers will struggle to continually pass growing costs on to consumers and so must find a way of minimizing claims and operating costs. Otherwise, a repeat of 2023—in which the only winners seem to have been PCWs—appears a certainty.