GlobalData surveying has found that larger-sized SMEs are more likely to use credit to pay for their insurance purchases. Meanwhile, research from Premium Credit has found that the number of SMEs using credit to purchase insurance is growing.

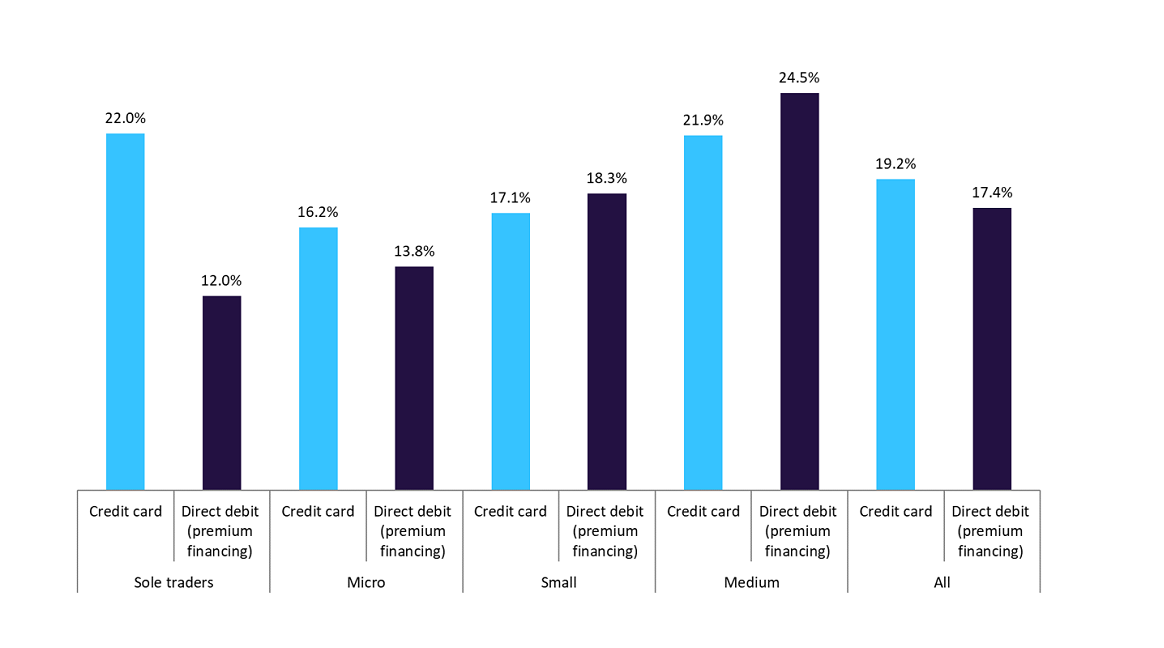

GlobalData’s 2023 UK SME Insurance Survey has found that medium-sized SMEs are more likely to utilise credit to manage their insurance expenses, with 21.9% opting for credit card payments and 24.5% choosing direct debit (premium financing). Conversely, smaller-sized businesses, such as sole traders or micro-sized firms, exhibit a lower propensity to use credit for insurance. For example, 16.2% of micro-sized businesses utilized credit card payments while 13.8% engaged in monthly direct debit (premium financing). This suggests that larger SMEs are more inclined to leverage credit options (credit card or premium financing) for insurance payments compared to smaller-sized businesses, indicating potential differences in financial strategies and risk management practices across various SME segments.

Go deeper with GlobalData

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

Medium-sized SMEs, with potentially larger revenue streams and more complex operational structures, may find it more feasible to leverage credit options such as credit card payments to manage insurance expenses. In contrast, smaller businesses, such as sole traders or micro-sized firms, may operate on tighter budgets and prefer alternative, less credit-dependent methods for insurance payments, reflecting their cautious approach to financial management and risk mitigation.

Meanwhile, research from Premium Credit has found that the number of SMEs using credit to pay for their insurance has increased in the past year, with nearly one in five of them increasing the amount they borrow. Premium Credit’s Insurance Index, which monitors insurance buying and how it is financed, shows 55% of SMEs now use some form of credit to pay for insurance. This represents a four-percentage-point increase when compared to the prior year.

The rise of SMEs resorting to credit for insurance payments can be attributed to the broader economic trend of increasing costs and premiums. Insurers often adjust their premiums to account for higher operational costs and potential increases in claim payouts due to inflationary pressures. As a result, businesses may find it challenging to manage these rising insurance expenses within their existing budgets. Consequently, they may turn to credit as a means to bridge the financial gap between their immediate cash flow and the mounting costs of insurance coverage. This reliance on credit enables SMEs to remain protected while mitigating the strain caused by inflation-induced premium hikes on their finances.

Insurers can assist SMEs facing rising costs and premiums by offering flexible payment options, such as instalment plans or deferred payment arrangements, to alleviate immediate financial strain. They can also provide tailored insurance packages that align with SMEs’ specific needs, optimising coverage while minimizing costs.