Wearable technology allows for more-accurate underwriting and over half of US consumers would be willing to share data collected from such devices with a life insurer, as per a GlobalData survey. However, to seize the opportunity to its full potential, insurers will need to overcome existing challenges, such as privacy concerns.

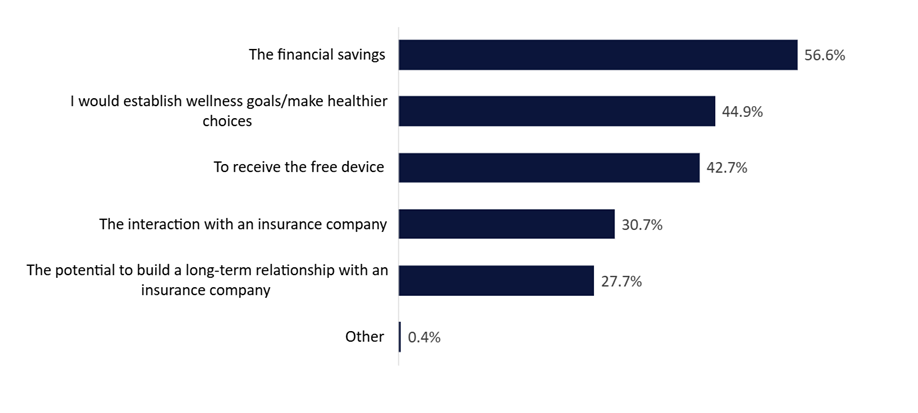

According to GlobalData’s 2024 Emerging Trends Insurance Consumer Survey, over half of US consumers (54.5%) would be quite or very likely to consider wearing an activity tracker (or biotech accessory) and sharing the results with a life insurer or private medical insurer in return for a more-tailored policy. This proportion is significantly higher than the 20.7% of consumers who would be reluctant to share their data with an insurer. The prospect of financial savings is the main incentive (56.6%) for sharing such data, yet a substantial proportion of consumers (44.9%) would do so for their own health and wellness benefit, such as to establish wellness goals or make healthier choices.

Go deeper with GlobalData

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

Wearable technology allows for more-accurate underwriting and over half of US consumers would be willing to share data collected from such devices with a life insurer, as per a GlobalData survey. However, to seize the opportunity to its full potential, insurers will need to overcome existing challenges, such as privacy concerns.

According to GlobalData’s 2024 Emerging Trends Insurance Consumer Survey, over half of US consumers (54.5%) would be quite or very likely to consider wearing an activity tracker (or biotech accessory) and sharing the results with a life insurer or private medical insurer in return for a more-tailored policy. This proportion is significantly higher than the 20.7% of consumers who would be reluctant to share their data with an insurer. The prospect of financial savings is the main incentive (56.6%) for sharing such data, yet a substantial proportion of consumers (44.9%) would do so for their own health and wellness benefit, such as to establish wellness goals or make healthier choices.

Why would you consider wearing an activity tracker (or biotech accessory) and sharing the results with a life or private medical insurance company? US, 2024

Note: Respondents could select all options that applied to them.

Source: GlobalData’s 2024 Emerging Trends Insurance Consumer Survey

US Tariffs are shifting - will you react or anticipate?

Don’t let policy changes catch you off guard. Stay proactive with real-time data and expert analysis.

By GlobalDataThe incorporation of wearable technology can have a significant impact on the insurance industry. Devices (such as smartwatches and fitness trackers) collect real-time health and lifestyle data that, when shared with insurers, can be used to assess risks and price policies more accurately, while the devices also offer a novel way of engaging with customers.

In this respect, WTW has recently partnered with the UK-based health data analytics company Klarity to launch a new life insurance underwriting model leveraging wearable technology. It will use Klarity’s mortality risk profiles, developed using 12 years of health data from wearables. WTW verified Klarity’s model using official US health and nutrition data, finding it provided more-granular segmentation.

Using new models based on wearable data can address shortcomings in traditional underwriting, which has traditionally relied on health and lifestyle indicators, such as cholesterol, blood pressure or tobacco use. In contrast, using more-robust data and additional indicators, including resting heart rate, sleep quality, and activity levels, can lead to get a more-accurate picture of an individual’s health and lifestyle. It enables for a more-personalized policy with more-accurate pricing based on the individual’s own risk. Moreover, by analyzing robust large datasets from wearables, insurers can identify potential health issues early on and offer personalised health tips to mitigate risks; taking a more-preventative approach.

Yet, further findings from the survey reveal that the most-common reasons among those unlikely to share data with an insurer are the perception that it is sharing too much data (53.8%), privacy concerns (53.8%), and just would not be willing to wear a device (50%). These are the main challenges that insurers will have to overcome to improve outreach and make the most of novel models incorporating wearables.