UK brokers believe cyber insurance is the new or emerging commercial insurance product with the most growth potential, as per a GlobalData survey. Significantly low cyber insurance penetration rates among smaller firms make SMEs a largely untapped market for growth.

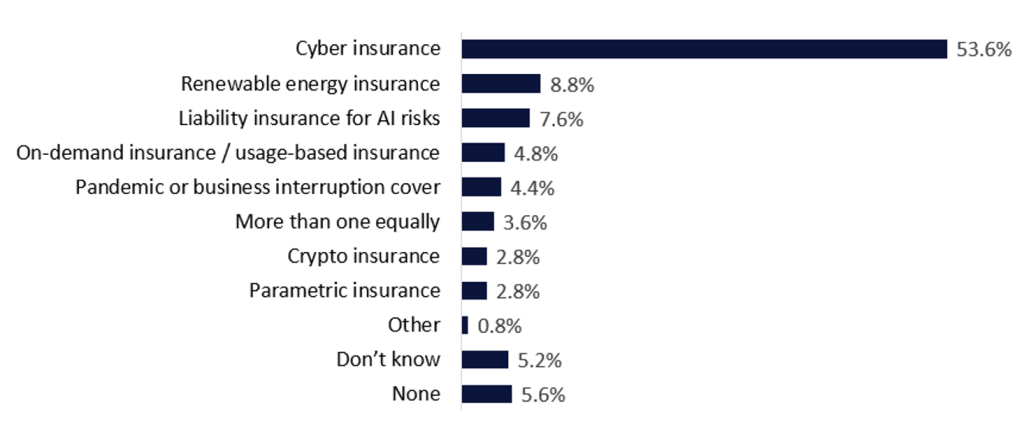

According to GlobalData’s 2025 UK Commercial Insurance Broker Survey, over half of brokers (53.6%) believe cyber insurance has the potential to record the strongest growth among new or emerging commercial insurance products. Cyber insurance significantly surpasses the potential of other emerging products, with renewable energy insurance—the second-most popular product—attaining 8.8% of responses.

Which new or emerging commercial insurance product do you see as having the most growth potential? 2025

GlobalData’s findings are supported by recent research published by Aon. Its Reinsurance Market Dynamics: Midyear 2025 Renewal report finds that reinsurance capacity is poised to support growth in the global cyber insurance market as reinsurers diversify their strategies to tap into emerging risks. Greater appetite around this line of business will help softening market conditions, as an increase in capacity can help insurers combat soaring premiums.

Despite the growing awareness of cyber risks among businesses, the adoption of cyber insurance is not universal, with underinsurance remaining a key challenge to the industry. The protection gap is more pronounced among smaller businesses, with GlobalData’s 2025 UK SME Insurance Survey revealing that 60.8% of SMEs do not hold such cover. The most common reason for not holding cyber insurance is because businesses believe it is unlikely that they will be a target of a cyberattack, as cited by 40.5% of SMEs. Yet the likelihood of a cyberattack is six times greater than an event impacting property, according to Aon.

Insurers will need to tackle the protection gap through several fronts to grow the cyber insurance market. Focusing on conveying the impact that a cyberattack can have on a business—not only in terms of operations, but also reputation—can be beneficial. Equally, there could be greater transparency on policy wording, making it clearer what the perils and exclusions are to avoid this being a barrier to buyers. Lastly, SMEs remain a largely untapped market and are often more vulnerable to attacks but have fewer resources to respond effectively. This makes them strong candidates for tailored cover, developing products that address their specific needs.

Go deeper with GlobalData

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.