Aviva’s £3.7bn acquisition of Direct Line is set to finalise in July 2025 and the combined group is expected to become a major force in the UK’s general insurance sector as per GlobalData’s analytics. Aviva is willing to take a risk and proceed with the deal ahead of receiving Competition and Markets Authority (CMA) clearance.

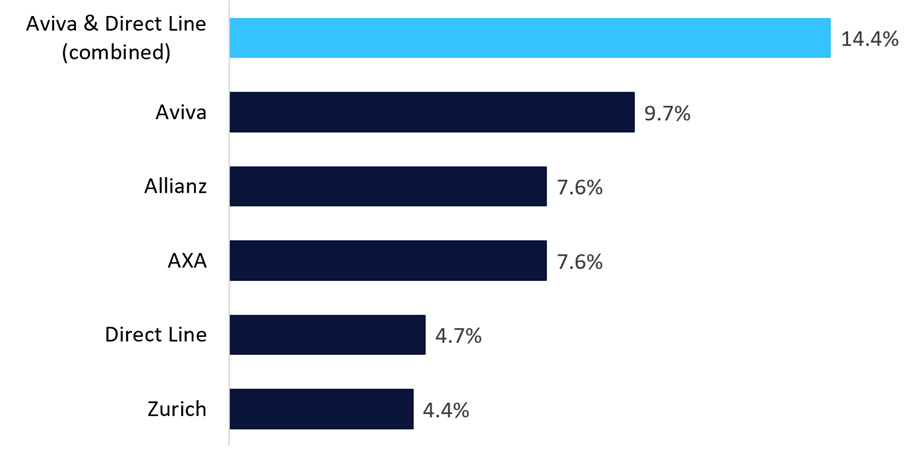

Aviva is the largest general insurance player in the UK; accounting for 9.7% of GWP in 2023 as per GlobalData’s UK Top 25 General Insurance Competitor Analytics. Aviva has a healthy lead over Allianz and AXA; the joint-second-largest players which each control 7.6% of the market. Aviva’s position as the leading player will strengthen significantly upon the acquisition of Direct Line, with the combined group potentially almost doubling the joint-second-largest player’s market share (14.4%). In particular, the greatest advancements will be in the motor insurance space, where Aviva could end up controlling roughly a fifth of the market (19.6%). It would also command a significant share of the total UK property insurance market (17.3%).

Go deeper with GlobalData

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

Top players in the UK general insurance market by GWP, 2023

Aviva’s acquisition of Direct Line is a significant event for the UK general insurance market and it is now approaching its final stages. The proposed acquisition has so far gotten regulatory approvals by both the Financial Conduct Authority (FCA) and the Prudential Regulatory Authority (PRA) and is now pending clearance from the CMA. The finalisation of the deal is expected around 1 July 2025, following a High Court Sanction hearing; given that Aviva has waived CMA clearance. With Aviva expressing confidence that the takeover will go ahead, it is willing to proceed with the acquisition ahead of the CMA’s formal decision if the High Court Hearing sanction is favourable. This makes the High Court Sanction hearing a crucial date. Aviva’s decision to not wait to receive the CMA’s decision signals confidence that it will receive unconditional clearance, while also shows keen interest in expediting the deal. Unlike some jurisdictions, the UK’s merger control system is non-suspensory; implying that a transaction can be completed before the CMA gives the green light. However, this is not risk free as remedial measures would need to be taken if the CMA concluded that the scale of the combined group would result in a substantial lessening of competition in the market. If that were the case, the CMA could impose remedies (such as divestitures) to lessen the impact, which could be detrimental to Aviva’s reputation. Under the acquisition proposal,

Direct Line’s brands such as Churchill and Darwin Motor Insurance will all now fall under Aviva’s umbrella. In any case, the resulting larger combined group could benefit from operational efficiencies, which may potentially reduce costs for Aviva and may result in more-favourable premium rates for customers. At the same time, having a dominant player in the market may end up reducing the number of major competitors; thereby limiting consumer choice. Meanwhile, the proposed merger has already had repercussions with top executives at Direct Line stepping down from their position and fears arising about potential job losses upon completion of the takeover.