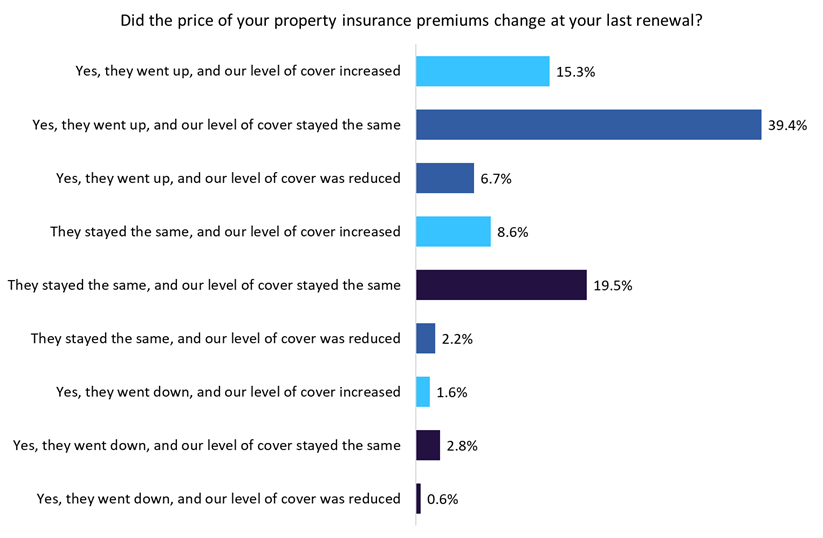

Findings from GlobalData’s 2022 UK SME survey suggest that almost half of UK SMEs are facing higher commercial property insurance premiums for the same or a lower level of cover than in 2021. Another quarter of SMEs have increased their level of commercial property cover, helping to eliminate at least some of the underinsurance in the sector.

The commercial property insurance sector faces a series of difficult challenges as growing repair costs, the greater likelihood of adverse weather events, and the lingering threat of belated business interruption claims heighten risks and drive premium increases in the line. Our 2022 UK SME Insurance Survey indicates that 48.3% of UK SMEs are facing higher premiums in relation to their level of cover in 2022 compared to the previous year.

Go deeper with GlobalData

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

As the cost-of-living crisis continues in the UK, a growing number of SMEs may soon lose the capacity to afford an insurance product that offers less protection despite increasing threats. Indeed, 52% of SMEs surveyed indicated that they are, to some extent, concerned about the impact of the cost-of-living crisis on their business. Given these concerns and challenges in the sector, some SMEs may seek more tailored or flexible insurance property cover going forward. This will enable SMEs to reduce costs while ensuring cover remains in case of emergency.

Source: GlobalData’s 2022 UK SME Insurance Survey

Our survey also indicates that a significant proportion of SMEs (25.5%) have sought to increase their level of property cover as inflation bites and the pitfalls of underinsurance become more apparent. SMEs may find that policies become (at best) insufficient or (at worst) invalidated depending on the level of underinsurance. Alleviating these concerns can reduce the potential impact of adverse weather or major claims (such as fire). The industry has clearly done well to educate clients in this regard, with the cost-of-living crisis likely reducing the number of SMEs that would have increased cover if they could. Given that 46.1% of SMEs are paying higher premiums than in 2021 for the same level or less cover, it is likely that these firms would have been able to afford extra capacity had the hardened market rates not further priced them out.

Overall, these findings are suggestive that the market is reacting in the right way to combat underinsurance. However, the cost-of-living crisis is getting in many firms’ way of minimising this risk. As inflation cools over 2023 and beyond, insurers should maintain that SMEs’ property cover be increased, helping to bring overall protection to more appropriate levels in the near future.