The UK government has plans to increase both the age at which individuals can access their private pensions and the age at which they can claim state pension pay. Given the low state pension pay and the government’s initiatives to shift the burden of retirement income to individuals, consumers are now more concerned about an increase to the private pension access age than having to wait for longer to receive state pension pay.

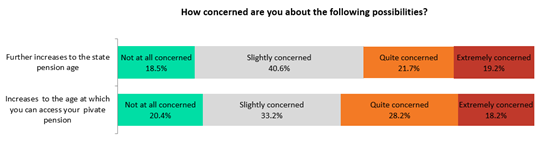

According to GlobalData’s 2022 UK Life and Pensions Survey, 46.4% of all consumers feel either quite concerned or extremely concerned about the prospect of an increase to the age at which they can access their private pension. The proportion of individuals expressing this level of concern regarding further increases to the state pension age is also high at 40.9%.

Go deeper with GlobalData

State pension pay is notoriously low in the UK, with the maximum standing at GBP185.15 ($227) – although not everyone receives this amount. While many individuals will rely on this pay as a source of income in retirement to some extent, other sources such as savings, private pensions, and investments are normally needed to supplement this. Nonetheless, given individuals’ propensity to retire at around the state pension age (SPA), and the fact that private pensions can be accessed earlier in life than the SPA, the findings are significant. They highlight that individuals now see private pensions as an important component of their retirement income. Indeed, the government’s introduction of auto-enrolment was intended to facilitate saving into private pensions and lower the reliance on the state pension.

The age at which individuals can start claiming the state pension has already been increased several times to reflect that life expectancy has risen over the years. There are plans to continue increasing this age. The SPA for all individuals is 66 since October 2020, and this is set to increase to 68 by 2039. Meanwhile, private pensions can normally be accessed from the age of 55, but the government plans to increase this age to 57 in the coming years.

While people are living longer, there is a lag of several years between life expectancy and healthy life expectancy, which is the average age at which individuals develop serious health conditions that may prevent them from working altogether. Data from the Office for National Statistics shows that healthy life expectancy sits at 62.8 years in the UK – lower than the SPA. This should highlight further opportunities to educate individuals on the importance of long-term savings, including through private pensions. Financial advisors and brokers will have a key role to play in this respect.

US Tariffs are shifting - will you react or anticipate?

Don’t let policy changes catch you off guard. Stay proactive with real-time data and expert analysis.

By GlobalData